16 Core Money Rules That Will Transform Your Financial Future: The Ultimate Guide to Building Lasting Wealth

Most people never learn the fundamental principles that separate those who build lasting wealth from those who spend a lifetime chasing it. These aren't secrets locked away in Ivy League classrooms or reserved for Wall Street insiders — they're timeless financial principles that anyone can apply starting today.

The problem? Nobody teaches them in school. And that's not an accident.

In this comprehensive guide, we break down 16 essential money rules across four critical pillars: cognition and compounding, risk management, asset allocation, and investment psychology. Whether you're just starting your financial journey or looking to refine your strategy, these rules will fundamentally change how you think about money.

Part 1: Cognition & Compounding — The Foundation of Wealth

Rule 1: The Compound Effect

A snowball starts small. But keep it rolling long enough and it becomes unstoppable. Your money works exactly the same way.

The secret isn't how much you invest — it's how early you start.

Consider this: someone who invests $200 per month starting at age 25 will have significantly more wealth at 65 than someone who invests $400 per month starting at age 35 — even though the late starter invested more total money. That's the compound effect in action.

Albert Einstein reportedly called compound interest "the eighth wonder of the world." Whether he actually said that or not, the math is undeniable:

- $10,000 invested at 8% for 10 years → ~$21,589

- $10,000 invested at 8% for 20 years → ~$46,610

- $10,000 invested at 8% for 30 years → ~$100,627

The Rule of 72 provides a quick mental shortcut: divide 72 by your annual return rate, and you get the approximate number of years needed to double your investment. At 8%, that's roughly 9 years.

Core Principle: Time is your most powerful wealth-building weapon. Start now, even if the amount is small.

Rule 2: Money Illusion

That $100 in your wallet? It was worth more last year. And even more 10 years ago. The number stays the same — but what it buys keeps shrinking.

This is the money illusion — the tendency to think about money in nominal terms (the number) rather than real terms (purchasing power). In 2025, central banks target around 2% inflation, but real-world costs for housing, healthcare, and education often rise much faster.

Here's what inflation does to $100,000 sitting in a savings account earning 0.5%:

| Years | Purchasing Power (at 3% inflation) |

|---|---|

| 5 | ~$85,873 |

| 10 | ~$73,742 |

| 20 | ~$54,379 |

| 30 | ~$40,101 |

Your money isn't "safe" sitting still. It's actively losing value every single day.

Core Principle: Inflation silently steals your buying power. Your investments must outpace it.

Rule 3: Sunk Cost Fallacy

You bought a stock. It dropped 40%. You hold on because "I've already lost so much." That thinking will cost you even more.

The money is gone. Your next decision shouldn't be held hostage by it.

The sunk cost fallacy is one of the most psychologically powerful traps in investing. It manifests in many ways:

- Holding a losing stock because you "can't afford to sell at a loss"

- Continuing to pour money into a failing business because you've "invested too much to quit"

- Keeping a subscription you never use because you already paid for the year

Professional investors apply a ruthless test: "If I had this money in cash right now, would I buy this asset at today's price?" If the answer is no, the rational move is clear — regardless of what you originally paid.

Core Principle: Money already spent should NEVER drive your next decision. Cut your losses and deploy capital where it has the best future return.

Rule 4: Opportunity Cost

Every dollar you spend is a dollar that didn't grow. Every time you choose A, you give up what B could have returned.

Spending isn't just losing money — it's losing future money too.

The concept of opportunity cost is especially powerful when combined with the compound effect. That $5 daily latte isn't just $1,825 per year. Over 30 years, invested at 8%, that's over $200,000 in foregone wealth.

This doesn't mean you should never enjoy life. It means you should make conscious trade-offs:

- A $50,000 new car vs. a $25,000 reliable used car — the $25,000 difference invested could become $250,000+ over 20 years

- A $500/month apartment upgrade vs. investing the difference — that's potentially $500,000+ over 25 years

- Impulse purchases vs. a 48-hour cooling-off rule — most "urgent" wants disappear within two days

Core Principle: Choosing A means giving up what B could have earned you. Make every financial choice with full awareness of what you're sacrificing.

Part 2: Risk Control & Balance — Protecting Your Wealth

Rule 5: The Risk-Return Rule

There is no free lunch. Anyone offering low risk AND high reward is either lying or selling something.

The higher the potential gain, the higher the danger. Always.

This is perhaps the most important rule to internalize because it protects you from scams, Ponzi schemes, and too-good-to-be-true investment offers. Every asset class follows this fundamental law:

| Asset Class | Expected Return | Risk Level |

|---|---|---|

| Government Bonds | 2-4% | Low |

| Corporate Bonds | 4-6% | Low-Medium |

| Blue-Chip Stocks | 7-10% | Medium |

| Small-Cap Stocks | 10-14% | Medium-High |

| Venture Capital | 15-30% | Very High |

| Cryptocurrency | Highly Variable | Extreme |

When someone promises 50% annual returns with "no risk," run the other way.

Core Principle: Higher returns ALWAYS come with higher risk. If something sounds too good to be true, it is.

Rule 6: The Law of Large Numbers

One coin flip means nothing. One thousand coin flips tells you everything.

The more consistently and broadly you invest, the closer your results get to the expected outcome. This is why time in the market beats timing the market — with enough data points, volatility smooths out and the underlying growth trend emerges.

Consider the S&P 500:

- Any single day: ~53% chance of being positive

- Any single year: ~73% chance of being positive

- Any 10-year period: ~94% chance of being positive

- Any 20-year period: Historically 100% positive

The math is clear. Consistency and patience are your greatest statistical advantages.

Core Principle: Invest more often and wider — your results will trend toward your target over time.

Rule 7: Volatility ≠ Risk

Your portfolio dropping 15% this month is NOT a loss — unless you sell.

Short-term noise is not long-term damage. The real risk is panic, not price swings.

This distinction separates successful long-term investors from those who buy high and sell low. Consider the 2020 market crash:

- March 2020: S&P 500 dropped ~34% in just one month

- December 2020: S&P 500 had fully recovered and hit new all-time highs

- Those who sold in March locked in real losses

- Those who held (or bought more) benefited enormously

True risk isn't temporary price fluctuation. True risk is:

- Permanent capital loss (the company goes bankrupt)

- Inflation erosion (your returns don't keep up with price increases)

- Behavioral mistakes (selling during panics, buying during euphoria)

Core Principle: Temporary price swings are NOT permanent losses. Stay the course.

Rule 8: Margin of Safety

A bridge built to hold 10 tons that only ever carries 5 tons — that's a safe bridge.

Buy assets below their real value and you've built that same buffer into every investment. This concept, popularized by Benjamin Graham and championed by Warren Buffett, is the cornerstone of value investing.

The margin of safety protects you against:

- Errors in your analysis (nobody's valuation is perfect)

- Unexpected market events (pandemics, wars, recessions)

- Normal business fluctuations (revenue shortfalls, cost overruns)

In practical terms, if you estimate a stock is worth $100, don't buy it at $95. Wait until it's available at $70 or less. That 30% discount is your margin of safety — your insurance against being wrong.

Core Principle: Buying below intrinsic value is your greatest protection against uncertainty.

Part 3: Allocation & Diversification — Building the Right Portfolio

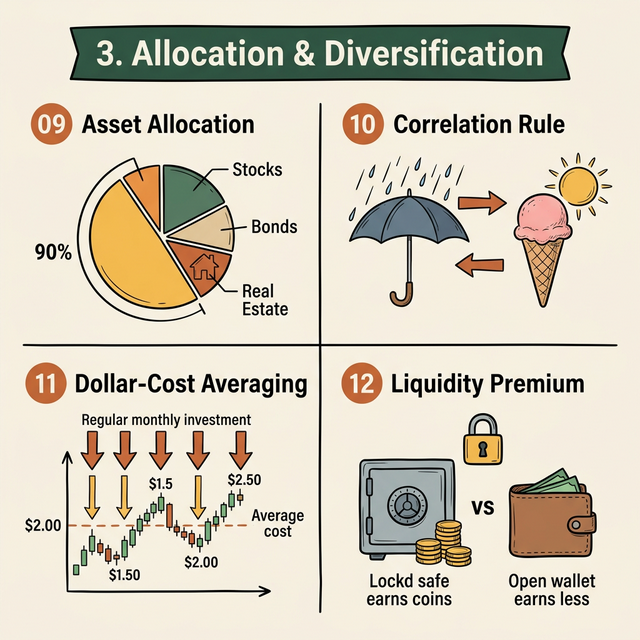

Rule 9: Asset Allocation

Research shows that asset allocation — not stock picking — determines up to 90% of your long-term returns.

It's not about finding the best stock. It's about building the right mix.

The famous Brinson, Hood, and Beebower study found that the decision of how to allocate between stocks, bonds, real estate, and other asset classes accounts for the vast majority of portfolio performance variation. Yet most investors spend 90% of their time on the 10% that matters least (picking individual securities).

A well-constructed allocation might look like:

For a 30-year-old with high risk tolerance:

- 70% Equities (mix of domestic and international)

- 15% Real Estate (REITs or direct)

- 10% Bonds

- 5% Alternatives (commodities, crypto)

For a 55-year-old approaching retirement:

- 40% Equities

- 25% Bonds

- 20% Real Estate

- 10% Cash/Money Market

- 5% Alternatives

The key principle: your allocation should reflect your time horizon, risk tolerance, and financial goals — not the latest hot tip.

Core Principle: How you allocate across asset classes decides 90% of your total returns.

Rule 10: The Correlation Rule

When it rains, umbrellas sell. When it's sunny, ice cream sells. Hold both.

Assets that move in opposite directions protect you when one side crashes. This is the essence of diversification — not just owning many things, but owning things that behave differently under different conditions.

Key correlation insights:

- Stocks and bonds often move inversely during market stress

- Gold tends to rise when equities fall and during inflationary periods

- Real estate has its own cycle, partially independent of stocks

- International equities can zig when domestic markets zag

The goal isn't to eliminate all volatility. It's to ensure that when one part of your portfolio is struggling, another part is providing stability or growth.

Core Principle: Hold assets that don't move together to reduce your overall portfolio risk.

Rule 11: Dollar-Cost Averaging (DCA)

Stop trying to time the market. Just invest the same amount every month — automatically.

When prices are high, you buy fewer shares. When prices are low, you buy more shares. Over time, your average cost beats the person who waited for the "perfect" moment — because that moment never comes.

Here's why DCA works:

| Month | Share Price | $500 Investment | Shares Bought |

|---|---|---|---|

| Jan | $50 | $500 | 10.0 |

| Feb | $40 | $500 | 12.5 |

| Mar | $30 | $500 | 16.7 |

| Apr | $45 | $500 | 11.1 |

| May | $55 | $500 | 9.1 |

| Total | Avg: $44 | $2,500 | 59.4 shares |

If you had waited and invested all $2,500 in January at $50, you'd have 50 shares. With DCA, you got 59.4 shares for the same total investment. Your average cost per share: $42.09 vs. $50.

Core Principle: Invest regularly and automatically to spread your cost and remove emotion from the equation.

Rule 12: Liquidity Premium

A locked safe earns more than an open wallet. The harder it is to access your money, the more return you get for that sacrifice.

Not all money should be easy to reach. This principle explains why:

- CDs pay more than savings accounts (your money is locked for a term)

- Private equity outperforms public markets (your capital is illiquid for years)

- Real estate generates strong returns (you can't sell a house at the click of a button)

The strategic implication: structure your finances in tiers:

- Immediate access (3-6 months expenses): High-yield savings account

- Short-term (1-3 years): CDs, short-term bonds

- Medium-term (3-10 years): Diversified stock/bond portfolio

- Long-term (10+ years): Real estate, retirement accounts, private investments

Core Principle: Strategically sacrifice liquidity to earn higher returns on money you don't need immediately.

Part 4: Mindset & Cycles — The Psychology of Wealth

Rule 13: Mean Reversion

Markets don't stay at the top forever. They don't stay at the bottom forever either.

Like a pendulum, everything that swings too far eventually comes back to the middle. This is one of the most statistically robust phenomena in financial markets.

When a sector, asset, or market has dramatically outperformed its historical average, expect it to underperform going forward. When something has been crushed and is trading far below historical norms, expect eventual recovery.

Real-world examples:

- Tech stocks in 2000 soared to absurd valuations, then crashed ~78%

- Energy stocks in 2020 hit record lows during the pandemic, then surged 200%+ by 2022

- Real estate in 2006 reached unsustainable peaks, crashed, then recovered over the next decade

Core Principle: What rises too fast will fall. What falls too far will rise. Position accordingly.

Rule 14: Market Cycles

Markets have seasons. Winter is fear and cheap prices. Summer is greed and expensive prices.

The smartest investors plant in winter and harvest in summer. Understanding where you are in the cycle is one of the most valuable skills you can develop.

The four seasons of market cycles:

- Spring (Recovery): Economy bottoms, early investors enter, pessimism fades

- Summer (Expansion): Growth accelerates, confidence builds, everyone wants in

- Autumn (Peak): Euphoria, excessive risk-taking, "this time is different" mentality

- Winter (Contraction): Fear, panic selling, distressed assets create opportunity

The catch? Nobody rings a bell at the top or the bottom. But you can read the signs:

- When taxi drivers give stock tips → likely near a top

- When headlines scream "worst market ever" → likely near a bottom

- When everyone says "it can only go up" → danger zone

- When everyone says "it will never recover" → opportunity zone

Core Principle: Markets are seasonal — deploy capital during "winter" when assets are cheap, harvest during "summer" when they're expensive.

Rule 15: Circle of Competence

Warren Buffett passes on thousands of deals. Not because they're bad — but because they're outside what he truly understands.

Your circle doesn't need to be big. It just needs to be honest.

The circle of competence concept is about intellectual honesty. It means:

- Know what you know — and invest confidently within those boundaries

- Know what you don't know — and either learn deeply or stay away

- Beware of expanding your circle too quickly — overconfidence kills returns

If you understand technology companies because you work in tech, that's your edge. If you understand real estate because you've been a property manager, that's your edge. If you don't understand cryptocurrency beyond the hype, don't invest in it just because your neighbor made money.

The most dangerous investor is one who thinks their circle of competence is bigger than it actually is.

Core Principle: Only invest in what you truly understand. Clear boundaries matter more than breadth.

Rule 16: First Principles Thinking

Strip away the hype, the trends, the noise. Real wealth comes from one thing: supporting businesses that create real value.

That's it. Everything else is just packaging.

First principles thinking means going back to the fundamental truths:

- A stock is a piece of a real business

- A bond is a loan you make to someone

- Real estate is land and buildings people need

- Value comes from solving problems and serving needs

When you invest based on first principles, you stop chasing trends and start evaluating fundamentals:

- Does this business solve a real problem?

- Does it have a sustainable competitive advantage?

- Is management competent and aligned with shareholders?

- Is the price reasonable relative to the value being created?

Core Principle: Go back to the true source of wealth creation. Invest in businesses that solve real problems and create genuine value.

Pro Tips for Immediate Action

- Start compound interest NOW — even $50/month beats waiting for $500/month later

- Diversify across assets that move in opposite directions — stocks, bonds, real estate, commodities

- Apply the buy-back test: "Would I buy this at today's price?" If no, consider selling

- Invest in "winters" — when everyone is scared, opportunity is greatest

- Review your strategy annually — what worked last year may not fit this year

- Automate everything possible — remove emotion from recurring investment decisions

- Keep learning — financial literacy is the highest-ROI investment you'll ever make

The Hard Truths About Money

Before you go, internalize these uncomfortable realities:

- There is NO low-risk, high-reward investment — anyone promising that is lying or deluded

- Inflation is stealing 3–7% of your savings' value every single year — doing nothing IS a decision

- Most investors don't lose from bad markets — they lose from bad emotions — fear and greed are your worst enemies

- Short-term volatility is not the enemy — panic selling is — your biggest threat looks at you in the mirror

- Your circle of competence doesn't need to be large — it just needs to be honest — humility is a superpower in investing

Your 5-Step Quick Start Plan

Ready to apply these rules immediately? Here's your action plan:

- Save 20% of every paycheck before spending anything — pay yourself first

- Open a low-cost index fund (Vanguard, Fidelity, or Schwab) and let compound interest work

- Set up automatic monthly investing so emotion never blocks the trade

- Build 3-6 months of emergency cash first — that IS your margin of safety

- Only invest in what you can explain in one simple sentence — if you can't, you don't understand it well enough

Frequently Asked Questions

What is the most important money rule for beginners?

Start early and let compound interest work. Rule 1 (the Compound Effect) is the single most impactful principle. Even small amounts invested consistently over decades will grow to significant wealth thanks to exponential growth.

How much should I save each month?

A common guideline is the 50/30/20 rule: 50% of income for needs, 30% for wants, and 20% for savings and investments. However, the exact percentage matters less than consistency — saving 10% every month is better than saving 30% sporadically.

Is it better to invest a lump sum or use dollar-cost averaging?

Statistically, lump-sum investing beats DCA about two-thirds of the time because markets tend to go up over time. However, DCA reduces the psychological pain of investing and protects against catastrophically bad timing. For most people, DCA through automatic monthly contributions is the best practical approach.

How do I know if an investment is too risky?

Apply Rule 5 (Risk-Return Rule) and Rule 8 (Margin of Safety). If the promised returns seem disproportionately high relative to the risk, be suspicious. If you can't identify a clear margin of safety, the investment may be overpriced.

What should I invest in if I'm a complete beginner?

Start with low-cost, broad-market index funds (like those tracking the S&P 500 or total world stock market). They provide instant diversification, low fees, and exposure to the global economy. As you learn and grow your circle of competence, you can branch out into other asset classes.

How often should I review my investment portfolio?

Once per quarter at most, once per year at minimum. Checking too frequently leads to emotional reactions and unnecessary trading. Set your allocation, automate your contributions, and review periodically to rebalance.

Conclusion

Most people don't lose wealth because they earn too little. They lose it because nobody ever taught them these 16 rules.

The market rewards the patient, the informed, and the disciplined. It punishes the impulsive, the uninformed, and the emotional.

These rules aren't complicated. They don't require an MBA or a Bloomberg terminal. They require something much harder: consistency, patience, and the courage to think differently from the crowd.

Start simple. Stay consistent. Let time work for you.

Your future self will thank you.